Unlike most health clinics, a medspa's core services are GST/HST taxable: cosmetic procedures are excluded from the medical exemption even when a physician or nurse performs them. That means registering early, charging tax on treatments and retail, and claiming input tax credits on lasers, injectables and rent. The clean setup is Jane App for booking, charting and consents, paired with Xero for the books.

The quick version

Medspa bookkeeping in Canada sits in an unusual spot: the clinic looks like a health business, but the tax rules treat most of it like retail. Cosmetic services are taxable for GST/HST, injectables are inventory with real cost-of-goods-sold behaviour, and gift cards create liabilities most owners never book. Get those three things right and the rest is routine. This guide walks through the tax treatment, the mixed-supply problem, and the Jane App plus Xero workflow we set up for Canadian aesthetics clinics.

Why medspa services are GST/HST taxable

The medical exemption from GST/HST covers services provided for health care reasons. Since 2010, the rules have explicitly excluded services performed for cosmetic purposes, and that exclusion applies no matter who performs them. Botox for frown lines, dermal fillers, laser hair removal, chemical peels, microneedling and body contouring are all taxable, even in a physician-led clinic with nurse injectors. This is the opposite of the position most health practitioners are in (see our guides for chiropractors and therapists and counsellors, whose services are exempt).

The obligations are the standard ones: once your taxable revenue passes $30,000 over four consecutive calendar quarters, you must register and charge GST/HST. In practice, most medspas blow through that threshold in their first few months, so plan to register from the start. There is also a real upside: registering early, even voluntarily before you open, lets you claim input tax credits on the GST/HST you pay for lasers and devices, injectable stock, buildout, rent and software. On $150,000 of startup equipment, the recoverable tax is significant, and clinics that register late leave it on the table.

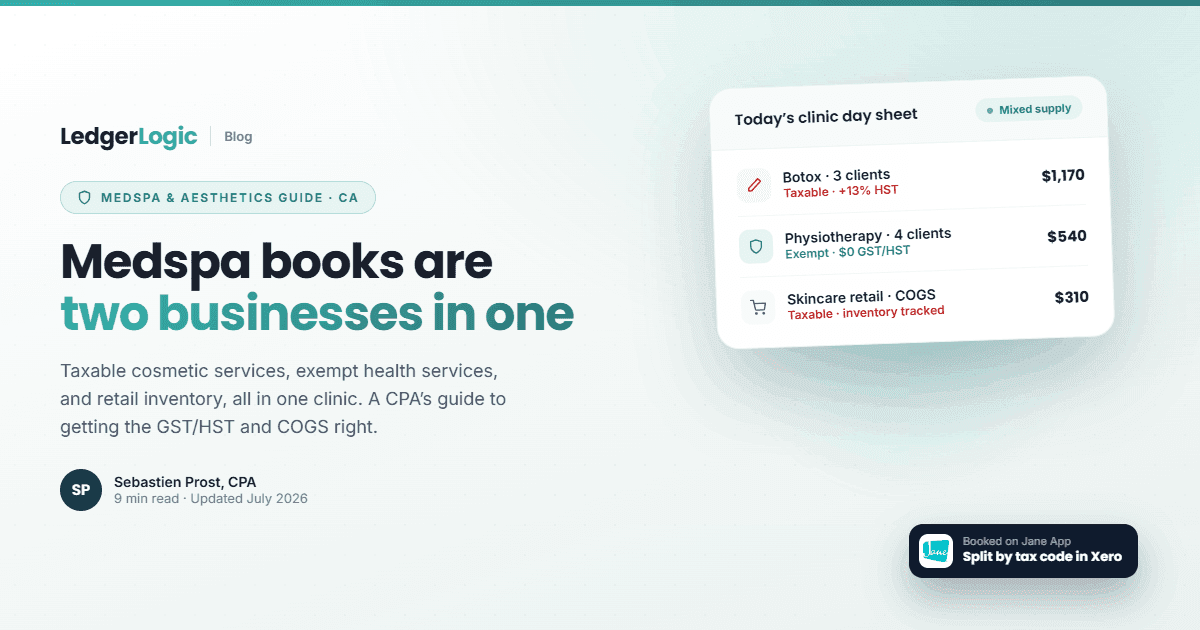

Mixed supply: when cosmetic and medical share a clinic

The tricky cases are clinics that do both. Botox billed for migraines or hyperhidrosis under a medical protocol can qualify as an exempt health service, while the same vial used cosmetically is taxable. A clinic that houses both a medical aesthetics practice and exempt services like physiotherapy or nursing care is running a mixed supply business: it charges GST/HST on the cosmetic side, does not charge it on the exempt side, and can claim input tax credits only on the portion of costs tied to taxable activity.

That apportionment is exactly the kind of thing the CRA looks at, so the bookkeeping requirement is documentation: each service coded as taxable or exempt at booking, the medical rationale recorded in the chart where an exempt treatment is claimed, and shared costs (rent, reception, software) apportioned on a defensible basis. If your clinic is purely cosmetic, you are spared all of this; everything is taxable and every input tax credit is claimable.

Injectables, retail and COGS

A medspa is one of the few clinic types with genuine inventory accounting. Injectables (neuromodulators and fillers) are purchased by the vial or syringe, and your margin per treatment depends on units used, wastage and pricing, so treat them as inventory with a cost-of-goods-sold account rather than expensing cases as they arrive. Tracking units per treatment in Jane against vials purchased in Xero is how you catch shrinkage and see the real margin on each service line. Skincare retail (cleansers, SPF, serums) is a second inventory stream with its own margin, always taxable, and worth splitting from services so you can see whether the retail shelf actually makes money.

Gift cards, packages and deposits

Aesthetics clinics sell more prepaid value than almost any other health business: gift cards, six-session laser packages, memberships and deposits. In the books, none of that is revenue when the money arrives. It is a liability (unearned revenue) that converts to revenue as sessions are delivered or cards are redeemed. Clinics that book gift card sales as income overstate revenue, understate their obligations, and get a nasty surprise when a busy December of gift card sales turns into a January and February of unpaid-for treatments. Jane tracks packages and remaining balances per client; your bookkeeper's job is to make Xero agree with Jane's outstanding-liability report every month.

The bookkeeping stack: Jane App plus Xero

The two-tool stack we recommend across clinics fits medspas particularly well. Jane App runs the clinic: online booking, charting with photos, consent forms that go out before the appointment, packages and memberships, and point-of-sale for retail. Xero runs the accounting: GST/HST tracking, inventory and COGS, bank reconciliation and year-end reports. Our Jane App review covers why it is our top pick for Canadian clinics, and the clinic management comparison stacks it against the alternatives. You can start Xero on a free trial whenever you are ready to set up the books.

Jane does not push data into Xero automatically, so once a month you export a revenue report from Jane and import it into Xero, mapping taxable services, exempt services (if any), retail and gift card movements to the right accounts. The step-by-step is in how to import Jane App sales into Xero, and the broader routine is in our guide to bookkeeping for a Jane App clinic. New to Jane? You can start with a free month using code LEDGERLOGIC1MO on our Jane App deal page.

Run Your Clinic on Jane, Free for a Month

Jane App handles booking, charting, insurance billing and payments for Canadian health clinics. Start with one month free using code LEDGERLOGIC1MO, then pair it with Xero for clean books.

What to track each month

- Service revenue by line: injectables, laser, facials and peels, each with GST/HST coded correctly, and exempt medical services split out if you offer them.

- Retail sales separate from services, with their own COGS.

- Injectable consumption: units used per Jane's treatment records against vials purchased, so COGS and shrinkage are real numbers.

- Gift card and package movements: sold (liability up), redeemed (liability down, revenue up), reconciled to Jane's outstanding balance report.

- Input tax credits on equipment, stock, rent and software, which is money back in a taxable clinic.

- Practitioner pay: nurse injectors and aestheticians on commission splits need the contractor-versus-employee call made correctly, because the CRA can reassess years of source deductions if a commissioned injector is really an employee. Jane's compensation reports handle the split math; a payroll tool like Wagepoint handles actual employees (compared in our payroll software guide).

Common bookkeeping mistakes medspas make

- Registering for GST/HST late. Most medspas pass $30,000 in months, not years, and late registration means uncollected tax plus forfeited input tax credits on startup costs.

- Booking gift card sales as revenue. Prepaid value is a liability until redeemed. December looks great, the new year pays for it.

- Expensing injectables with no COGS tracking. You cannot see per-treatment margin, wastage or shrinkage if vials go straight to expenses.

- Claiming exempt treatment without documentation. Botox for migraines is defensible when the medical rationale is charted; an undocumented exempt claim on a cosmetic treatment is a reassessment waiting to happen.

- Mixing personal and clinic money. The same rule as every clinic: a dedicated business account and card, no exceptions.

When to hire a bookkeeper

A medspa's books are more involved than most clinics from day one: sales tax on everything, two inventory streams, prepaid liabilities and commission payroll. A single-injector studio can manage with Jane, Xero and discipline, but the point to bring in help arrives fast: when you buy significant equipment (to capture the input tax credits properly), start selling packages and gift cards at volume, or run a mixed cosmetic-medical clinic that needs defensible apportionment. We do exactly this for Canadian aesthetics clinics, pairing Jane and Xero and keeping the books clean on a fixed monthly fee. You can see how that works on our bookkeeping service page.

Frequently asked questions

Do medspas charge GST/HST in Canada?

Yes. Services performed for cosmetic purposes are excluded from the GST/HST medical exemption, regardless of who performs them, so Botox, fillers, laser treatments, peels and body contouring are taxable. Once revenue passes $30,000 over four consecutive quarters you must register, and most medspas should register from day one to capture input tax credits on equipment and stock.

Is Botox taxable in Canada?

Cosmetic Botox is taxable for GST/HST. Botox administered for a medical purpose under a documented protocol, such as chronic migraines or hyperhidrosis, can qualify as an exempt health service. Clinics offering both must code each treatment correctly and keep the medical rationale in the chart for exempt claims.

Can a medspa claim input tax credits?

Yes, on costs tied to taxable activity, which for a purely cosmetic clinic is essentially everything: lasers and devices, injectable stock, buildout, rent and software. Mixed clinics with exempt medical services can claim input tax credits only on the taxable portion, apportioned on a defensible basis.

How should a medspa account for gift cards and packages?

As liabilities, not revenue. Money received for gift cards, prepaid packages and memberships is unearned revenue until the session is delivered or the card is redeemed. Reconcile the liability account in your books against Jane App's outstanding package and gift card balances each month.

What software do medspas use for bookkeeping?

Most Canadian aesthetics clinics run Jane App for booking, charting, consent forms, packages and retail point-of-sale, and Xero for the accounting. Jane does not sync directly to Xero, so you export a monthly revenue report and import it into Xero, mapping services, retail and gift card movements to the right accounts.

Are nurse injectors employees or contractors?

It depends on the working relationship, not the label. An injector who works your schedule, uses your equipment and stock, and serves your clients looks like an employee to the CRA, which means source deductions, T4s and records of employment. Genuine contractors invoice you and control their own work. Misclassification can trigger reassessment of years of unremitted deductions, so get this call right early.

Seb ProstCPA, Ex-CRA

Licensed CPA with 10+ years of experience, including work with the Canada Revenue Agency. Founder of LedgerLogic, a cloud accounting firm serving Canadian SMEs. Xero Certified Advisor.