Since June 2024, psychotherapy and counselling therapy services are GST/HST exempt for licensed practitioners, so most Canadian therapists no longer charge tax on sessions. The trade-off is that you generally cannot claim input tax credits on your expenses. The clean setup is Jane App for booking, telehealth and charting, paired with Xero for the books.

The quick version

Bookkeeping for therapists and counsellors in Canada changed meaningfully in 2024, and a surprising number of practitioners have not caught up. Psychotherapy and counselling therapy services became GST/HST exempt, which simplifies billing but quietly changes what you can claim, what you should charge on side income, and whether staying registered for GST/HST even makes sense. This guide walks through the tax treatment, the sole-prop-versus-corporation question, and the Jane App plus Xero workflow we set up for Canadian therapy practices.

The 2024 GST/HST exemption for psychotherapy and counselling

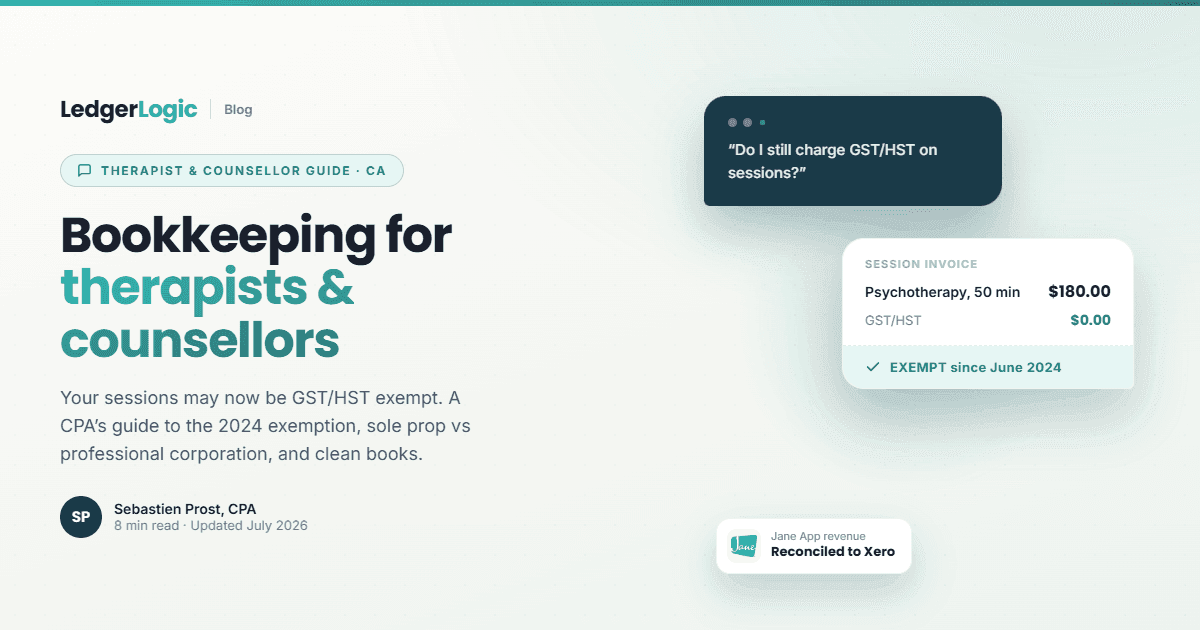

As of June 20, 2024, psychotherapy and counselling therapy services are exempt from GST/HST when delivered by a practitioner who is licensed or registered in a province that regulates the profession (for example, a Registered Psychotherapist in Ontario or a Counselling Therapist in the Maritimes), or who holds equivalent qualifications in a province that does not. Before that date, many therapists were charging GST/HST on every session; psychologists and social workers were already exempt under separate provisions, but psychotherapists and counsellors were not.

Two practical consequences follow. First, if you started practising after mid-2024, you likely never need to register for GST/HST for your session revenue at all, no matter how much you earn. Second, if you were registered before the change, you should have stopped charging tax on exempt sessions on the effective date, and for most practices it is worth deregistering so you are not filing nil returns forever. Charging GST/HST on an exempt service does not make it taxable; it just means you collected tax you were not supposed to, which is its own cleanup job. Confirm your registration status and effective dates with a CPA before you act, because the details depend on your province and your service mix.

The catch: no input tax credits, and taxable side income

Exemption sounds like a pure win, but it comes with the same trade-off chiropractors have lived with for years (we cover their version in bookkeeping for chiropractors): because you are not charging GST/HST, you generally cannot claim input tax credits on the GST/HST you pay for rent, software, supervision, insurance and equipment. That tax becomes part of your cost, so record expenses at their full GST/HST-inclusive amount.

The second wrinkle is that not everything a therapist sells is therapy. Workshops, webinars, corporate wellness sessions, clinical supervision of other therapists, and course sales are usually not exempt psychotherapy services, and they are taxable once you pass the $30,000 small-supplier threshold on that taxable side. A practice with $90,000 of exempt session revenue and $35,000 of workshop income has a GST/HST registration obligation most owners never see coming. Track the two streams separately from day one.

Sole proprietorship vs professional corporation

Most therapists start as sole proprietors, and for a part-time or early-stage practice that is the right call: income lands on your personal return, the bookkeeping is light, and there are no incorporation or annual filing costs. The equation changes as the practice grows. A professional corporation (available to regulated therapists in most provinces) pays the small business tax rate, roughly 9 to 12 percent combined on the first $500,000 of profit depending on your province, while you personally are taxed only on what you draw out as salary or dividends. If you consistently earn well more than you spend, the deferral is significant; if you draw out every dollar to live on, incorporation mostly adds cost and paperwork.

Our guide to the tax benefits and disadvantages of incorporating in Canada covers the full decision, and the small business tax rate numbers by province are here. The bookkeeping consequence of incorporating: you now need a separate business bank account, a real set of books, payroll if you pay yourself salary, and a corporate tax return, which is usually the point where doing it yourself stops being worth your evening.

The bookkeeping stack: Jane App plus Xero

For a Canadian therapy practice, the setup we recommend is the same two-tool stack we use across allied health. Jane App runs the practice: online booking, secure video telehealth (built in, PIPEDA-conscious, with data hosted in Canada), charting and session notes, intake forms, and receipts your clients can submit to their insurers. Xero runs the accounting: chart of accounts, bank reconciliation, and year-end reports. Our Jane App review explains why it is our top pick for Canadian clinics, and the clinic management comparison stacks it against the alternatives. You can start Xero on a free trial whenever you are ready to set up the books.

Jane does not push data into Xero automatically, so once a month you export a revenue report from Jane and import it into Xero. It is a 20 to 30 minute routine once you have a template; the step-by-step is in how to import Jane App sales into Xero, and the broader monthly routine is in our guide to bookkeeping for a Jane App clinic. New to Jane? You can start with a free month using code LEDGERLOGIC1MO on our Jane App deal page.

Run Your Clinic on Jane, Free for a Month

Jane App handles booking, charting, insurance billing and payments for Canadian health clinics. Start with one month free using code LEDGERLOGIC1MO, then pair it with Xero for clean books.

What to track each month

A therapy practice's books are simpler than a multi-practitioner clinic's, but a few streams still need to be kept apart:

- Exempt session revenue: individual, couples and group therapy, in person and telehealth. No GST/HST collected.

- Taxable side income: workshops, corporate sessions, supervision, courses. Tracked separately because it counts toward the $30,000 taxable threshold.

- Sliding-scale and no-show adjustments, recorded consistently so your revenue report matches what actually hit the bank.

- Expenses at full cost: rent, Jane and Xero subscriptions, association dues, liability insurance, supervision you pay for, continuing education. The GST/HST on these is generally not recoverable, so record the all-in amount.

- Insurance and third-party receipts (NIHB, Veterans Affairs, EAP programs) reconciled against actual deposits, since these often pay on their own schedule.

Common bookkeeping mistakes therapists make

- Still charging GST/HST on exempt sessions. If you were registered before June 2024 and never updated your invoicing, you have been collecting tax in error, and refunding or remitting it correctly is a cleanup job worth doing now.

- Claiming input tax credits after the exemption. Once your services are exempt, the GST/HST on your costs generally stops being recoverable. Claiming it invites a reassessment.

- Ignoring taxable side income. Workshops and supervision can quietly cross the $30,000 threshold and create a registration obligation on that slice of the practice.

- Mixing personal and practice money. A dedicated business account is the single biggest driver of clean, cheap bookkeeping, incorporated or not.

- Letting the Jane export pile up. Reconcile Jane to Xero monthly; a year of unreconciled sessions is where books go to die.

When to hire a bookkeeper

A solo therapist with exempt-only revenue can usually run the books with Jane, Xero and an hour a month. The complexity jumps at three points: when you incorporate (corporate books, payroll, a T2 return), when you add associates (contractor-versus-employee questions and split calculations, where a proper payroll tool like Wagepoint earns its keep, compared in our payroll software guide), or when taxable side income forces a partial GST/HST registration. At any of those points the sales-tax and payroll work is worth a professional. We do exactly this for Canadian therapy practices, pairing Jane and Xero and keeping the books clean on a fixed monthly fee; you can see how that works on our bookkeeping service page.

Frequently asked questions

Do therapists charge GST/HST in Canada?

Generally no, as of June 20, 2024. Psychotherapy and counselling therapy services are GST/HST exempt when delivered by a practitioner licensed or registered in their province, or with equivalent qualifications in an unregulated province. Psychologists and social workers were already exempt under separate provisions. Taxable side income such as workshops or supervision can still require registration, so confirm your mix with a CPA.

Should a therapist deregister from GST/HST after the 2024 exemption?

Often yes. If essentially all of your revenue is exempt psychotherapy or counselling, staying registered means filing returns with nothing to report and you generally cannot claim input tax credits anyway. If you keep taxable side income like workshops or supervision above the $30,000 threshold, you may need to stay registered for that portion. Review the timing with a CPA before deregistering.

Can a therapist claim input tax credits?

Generally not for expenses tied to exempt therapy services. The GST/HST you pay on rent, software, insurance and supervision becomes part of your cost. If you are registered because of taxable side income, you can claim input tax credits only on costs tied to that taxable activity.

Should a therapist incorporate in Canada?

Incorporate when you consistently earn well more than you draw out to live on. A professional corporation pays the small business rate (roughly 9 to 12 percent combined on the first $500,000 of profit, depending on province), which creates a meaningful tax deferral. If you spend everything you earn, incorporation mostly adds cost and filings. Most provinces allow regulated therapists to form professional corporations.

What software do therapists use for bookkeeping?

Most Canadian therapy practices run Jane App for booking, telehealth, charting and client receipts, and Xero for the accounting. Jane does not sync directly to Xero, so you export a monthly revenue report from Jane and import it into Xero, then reconcile against your bank deposits.

Is income from workshops and supervision taxable for GST/HST?

Usually yes. The 2024 exemption covers psychotherapy and counselling therapy services delivered to clients, not workshops, webinars, corporate wellness contracts, course sales or clinical supervision of other practitioners. Once that taxable income passes $30,000 over four consecutive quarters, you must register for GST/HST and charge tax on it.

Seb ProstCPA, Ex-CRA

Licensed CPA with 10+ years of experience, including work with the Canada Revenue Agency. Founder of LedgerLogic, a cloud accounting firm serving Canadian SMEs. Xero Certified Advisor.